Reports that the UK economy shrank in January 2025 is unlikely to be welcome news for the Chancellor, Rachel Reeves, as she struggles to get her ‘growth mission’ on track. According to Money Marketing, Britain’s Gross Domestic Product (GDP), which measures the UK’s economic activity, fell by 0.1% in the first month of the year.

The article also goes on to suggest that the UK economy may now be ‘in the slow lane’ after showing no sign of growth at the start of the year. In February, the Bank of England (BoE) slashed its growth estimate for the UK to 0.75%, half of its November 2024 estimate of 1.5% in November.

While that’s bad enough, the Financial Times also points to another BoE projection: inflation could continue to rise before it starts to drop. The bank’s predictions may not come as a surprise when you consider the Office for National Statistics (ONS) revealed inflation rose to 3% in January 2025, up from 2.5% the month before.

This increase, together with the lacklustre performance of the UK’s economy, could create a little-known financial phenomenon called ‘stagflation’. If it happens, it could have a significant impact on your household finances.

Read on to discover more about stagflation and the actions you could take that may help to protect your wealth from its effects.

Stagflation is an economic rarity

There is a very good reason you may not have heard of stagflation: it’s extremely unusual. To explain this, it’s worth explaining that ‘stag’ refers to a stagnant economy, and ‘flation’ refers to inflation.

Broadly speaking, inflation is driven by consumer demand, which means it increases when the economy is doing well. This is because consumers have the money and the confidence to spend more, which in turn, drives the economy forward.

During an economic downturn, consumers don’t tend to have the money or the confidence to spend as much, meaning inflation typically falls when the economy is stalling. With stagflation, you have higher levels of inflation at the same time as a stagnating economy.

The last time the UK struggled with severe stagflation was in the 1970s, when economic activity dropped significantly, and inflation soared to more than 20%.

Stagflation could reduce your wealth’s value in real terms

A key driver of stagflation is higher levels of inflation, which measures the rising cost of living over time. Consequently, £100 is likely to buy you less in the future than it does today, meaning your money’s value could suffer a significant fall in value in real terms.

To demonstrate this, you may want to consider the following. If you use the Bank of England’s inflation calculator, you’ll see that you need £173.35 in January 2025 to have the same spending power of £100 in January 2005.

This means your money needed to grow by more than 73% during the period just to keep pace with inflation. If it didn’t, it would be dropping in value in real terms.

Investing may help protect your wealth from stagnation’s effects

One way you might be able to combat this is to consider investing your money, as historically, the stock market has tended to provide greater long-term growth potential than cash savings.

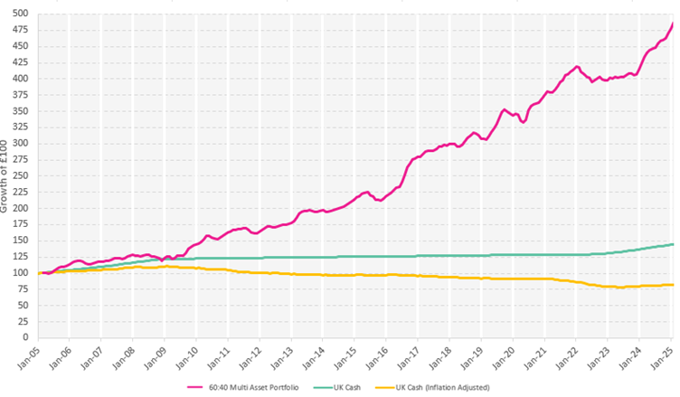

To demonstrate this, you might want to consider the following graph, which shows the performance of a medium risk 60:40 multi-asset portfolio between 1 January 2005 and 31 January 2025.

Data sourced from Morningstar by AFH Wealth Management. The 60:40 portfolio allocates 60% to MSCI ACWI and 40% to Bloomberg Global Aggregate.

As you can see, the multi-asset portfolio provided significantly higher levels of growth during the period, which in turn, could help to inflation-proof your wealth. Always remember that investing carries risk, and past performance is no guarantee of future performance. You may receive less than you originally invested.

A financial adviser will help you to understand the risks involved with investing, and whether it is likely to be the right option for you.

Get in touch

If you would like to discuss ways you could protect your wealth from stagflation, or would like to arrange a no obligation meeting with one of our advisers, please call us on 0333 010 0008 and we’d be happy to help.

Thursday 27 March 2025