According to the Office for National Statistics (ONS), inflation rose to 3% in January 2025 from 2.5% the month before. According to the BBC, the jump was partly driven by price rises across a range of items including meat, coffee, chocolate, bus and coach travel, air fares and private school fees.

When the ONS revealed the figures, Treasury minister James Murray said the road back to low inflation would be ‘bumpy’. That said, it wasn’t all bad news. According to the Beeb, some items fell in price, such as olive oil which dropped by a whopping 17%.

The fact that some rose in price while others dropped highlights an important point. Your personal rate of inflation could be very different to the ONS’s, which is an average based on a ‘basket’ of 700 goods that includes gas and electricity, bread, clothing and haircuts.

Understanding your personal rate of inflation could help you to better protect your wealth from its effects. Read on to discover how you could calculate your inflation rate, and why doing so could be a savvy financial strategy.

Before you do, we need to consider how inflation works and why it could significantly reduce the long-term value of your wealth in real terms.

Inflation measures the rising price of goods and services

Broadly speaking, inflation measures the rising cost of living over the long-term, which means it has the potential to affect everything from your weekly shop to your energy bills. As the cost of items goes up, your money buys you less in the future than it does today, meaning it’s falling in value in real terms.

To demonstrate the impact this could have on your household finances, you may want to consider the Bank of England’s inflation calculator. It reveals that you would need £177 in December 2024 to have the same spending power as £100 in December 2004.

In other words, your money needed to grow by 77% over the two decades to keep pace with the rising cost of living. If it didn’t, your money would have shrunk in real terms.

Your personal inflation rate depends on what you buy

Depending on how you spend your hard-earned cash, your personal rate of inflation could be significantly higher (or lower) than the ONS’s average rate. For example, if you fly abroad on a regular basis or have children at private school, it’s likely that your personal inflation rate will be higher.

The good news is that by working out your personal rate, you could identify where your spending is higher and adjust it to help mitigate the effects of inflation on your finances. To do this, you simply need to add up your current monthly spend and compare it to previous years.

For example, if your regular outgoings (not including one-off purchases) totalled £5,000 in December 2023, and £5,500 in December 2024, your personal inflation rate increased by 10% in the 12 months in between.

This comparison provides the opportunity to adjust your spending where possible, so that you can mitigate the effects of inflation on your finances. That said, there is another way you may be able to protect your money from the rising cost of living.

Investing could help to inflation-proof your cash

According to Moneyfacts, the top easy access savings account offered 4.75% interest on 19 February 2025, with the best five-year fixed rate offering 4.27%. While these are both above the ONS’s figure of 3%, it’s important to remember that your personal rate of inflation may be higher than these rates.

If it is, your money could be dropping in value in real terms. One way you might be able to combat this is to consider investing your money, as historically, the stock market has tended to provide greater long-term growth potential than cash savings.

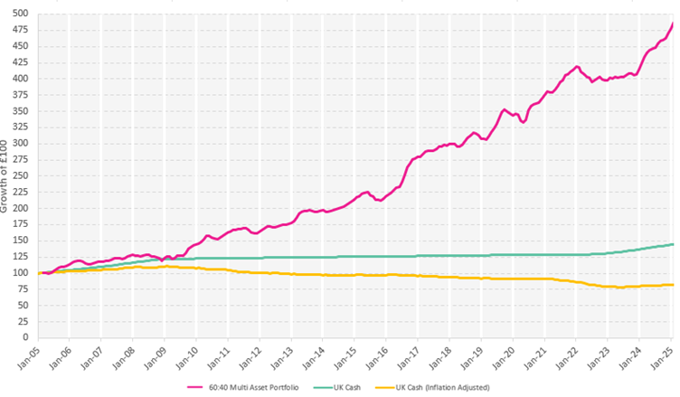

To demonstrate this, you might want to consider the following graph, which shows the performance of global equities and a medium risk 60:40 multi-asset portfolio between 1 January 2005 and 31 January 2025.

Data sourced from Morningstar by AFH Wealth Management. The 60:40 portfolio allocates 60% to MSCI ACWI and 40% to Bloomberg Global Aggregate.

As you can see, both the multi-asset portfolio provided significantly higher levels of growth during the period, which in turn, could help to inflation-proof your wealth. Always remember that investing carries risk, and past performance is no guarantee of future performance. You may receive less than you originally invested.

A financial adviser will help you to understand the risks involved with investing, and whether it is likely to be the right option for you.

Get in touch

If you would like to discuss ways to inflation proof your money or arrange a no obligation meeting with one of our advisers, please call us on 0333 010 0008 as we’d be happy to help.

Monday 10 March 2025